I’m offering an optional extra credit activity for students enrolled in Finance 4366. This opportunity involves attending and reporting on a presentation titled “The Campus Conformity Gauntlet” by Greg Lukianoff, the President and CEO of the Foundation for Individual Rights and Expression (FIRE). Mr. Lukianoff’s presentation is scheduled for Tuesday, April 23, beginning at 5:15 pm in Foster 240.

The presentation will discuss themes from Lukianoff’s recent book with Rikki Schlott, titled “The Canceling of the American Mind: Cancel Culture Undermines Trust and Threatens Us All-But There Is a Solution” (Simon & Schuster, 2023). It will examine how the suppression of free speech and the erosion of academic freedom, compounded by the pressure to conform in the realm of higher education, pose a significant threat not just to the academic community but to the very fabric of our democratic society.

Greg Lukianoff is not only the head of FIRE, but also a recognized attorney and author, with several New York Times bestsellers to his name. His notable works include “Unlearning Liberty: Campus Censorship and the End of American Debate,” “Freedom From Speech,” and along with NYU Professor Jonathan Haidt, “The Coddling of the American Mind: How Good Intentions and Bad Ideas Are Setting Up a Generation for Failure.” Lukianoff has also served as an executive producer on documentaries such as “Can We Take a Joke?” (2015), which examines the clash between humor, censorship, and the culture of outrage, and “Mighty Ira: A Civil Liberties Story” (2020), a documentary focusing on Ira Glasser, a former ACLU Executive Director.

If you take advantage of this opportunity, I will use the grade you earn on your report to replace your lowest quiz grade in Finance 4366. For this assignment, prepare a 2-3 page executive summary offering a thoughtful critique of Mr. Lukianoff’s presentation. To receive credit, the report must be submitted through Canvas in PDF format by 5 p.m. on Friday, April 26.

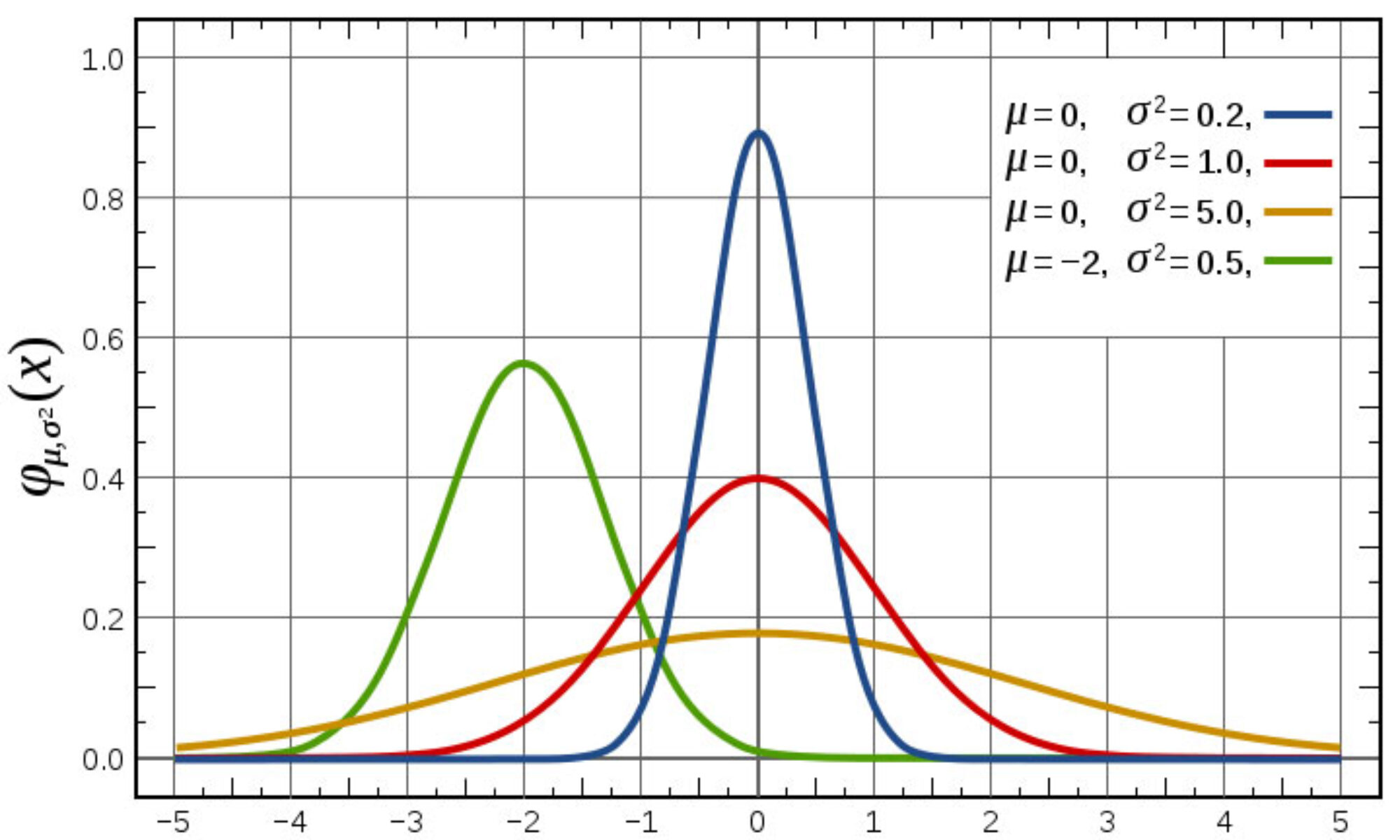

, while for problem 2,

, while for problem 2,  . Broadly, this sets the stage for examining the dynamics between the discrete-time Cox-Ross-Rubinstein (CRR) model and the continuous-time Black-Scholes-Merton (BSM) model, where

. Broadly, this sets the stage for examining the dynamics between the discrete-time Cox-Ross-Rubinstein (CRR) model and the continuous-time Black-Scholes-Merton (BSM) model, where  , and n corresponds to the number of time-steps that occur from the beginning of the binomial tree to the array of terminal nodes that exist at the expiration date T. As you will see toward the end of today’s lecture, CRR model prices and probabilities converge to BSM model prices and probabilities as the number of time steps becomes arbitrarily large.

, and n corresponds to the number of time-steps that occur from the beginning of the binomial tree to the array of terminal nodes that exist at the expiration date T. As you will see toward the end of today’s lecture, CRR model prices and probabilities converge to BSM model prices and probabilities as the number of time steps becomes arbitrarily large. becomes smaller. This leads to a corresponding decrease in the risk-neutral probability q and adjustments to the up (u) and down (d) factors.

becomes smaller. This leads to a corresponding decrease in the risk-neutral probability q and adjustments to the up (u) and down (d) factors.